March 2026

The month is closed, and not a great month as any self directed investor can attest to, given war rumblings and their impact on asset prices (unless you were fortunate enough to be overweight anything oil related).

Lots and lots and lots of experts out there on the macro feedback loop re: the war, and I am not one of them. I hope that one day, the entire world can find peace, but that is just a pipe dream these days.

For March, the S&P500 closed below it’s 200 day SMA, make of this what you will. I am assuming that this is as significant enough a monthly closing signal to potentially lead some asset managers to take notice. Presumably, some quantitative trend following strategies likely use the 200 day SMA as a regime filter.

It will be interesting to see how the next few months unfold. My cynical guess is, that the market continues down just enough to cause the 50 day SMA to cross below the 200 day SMA, at which point all of the mainstream pundits and strategists will trumpet a “death cross”, at which point, it will be closer to a buy signal than a fresh sell signal. When this occurs is anyone’s guess.

All of my quantitative systems use an index regime filter, and are coded to not take new trades when the index filter is off, and happily, I have seen this unfold in real time as I run my systems after the close each night. I am not happy about the down month, but I am happy that the systems I have designed are doing what they are supposed to be doing.

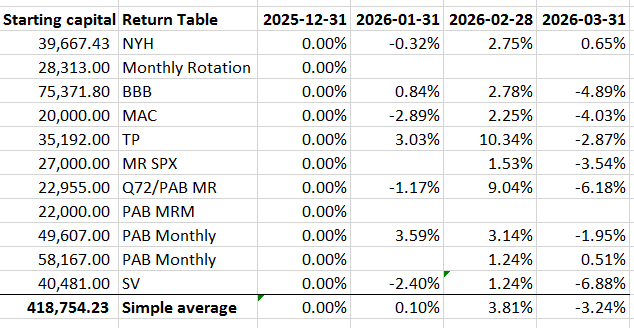

Here is the return table for March, based on today’s close across the various accounts and strategies I manage:

Some comments:

The worst performing accounts in March were the Q72 and Starvine strategies. Second worst were BBB, MAC, and Mean Reversion SPX. TP lost ground after a strong February. I am surprised that NYH posted a positive month.

I run the PAB monthly strategy in two separate accounts. The difference in performance was due to a couple of small differences between the accounts. In the $58,167 starting capital PAB Monthly account, I used KMLM not DBMF, so that led to slightly better performance. In the $49,607 starting capital PAB Monthly account, I had used a Russell 1000 and 3000 combined with SPY, which contributed to the worse performance in March in this account. Midway through the month, I exited the two incorrect ETF’s and entered SPY to ensure that the results match the signals and the asset mix more precisely.

The Starvine mirror account suffered due to overall market malaise and one of the overweight holdings taking a tumble post earnings.

I made one change during March, and I will apologize to Q72: I had trouble following this strategy. The signals are published weekly and I found that the mix of ETFs was hard to trade in real time, as was the slippage from Friday to Monday. One of the ETFs used had a very large spread, and trying to get fills was very challenging, exacerbated even more so by the March malaise. I made the decision to stop trading this strategy after a one week drop of over 5%, and in it’s place, I’ve added two separate mean reversion strategies offered by Price Action Lab Blog, Mean Reversion, and Mean Reversion Momentum Switching, so going forward, the table will track these mean reversion strategies. I also like the idea of adding a balance of long only trend following and mean reversion, so we shall see where this goes. I am treating my journey as a learning experience/real-time experiment.

A final bit of good news: my monthly rotation system generated its first signals as of the end of market close today, so tomorrow that system will put on its first trades: long GLD, IEF and XLU.

One final comment on psychology: the month of March was likely a difficult month for most investors. Most assets dropped, with the exception of anything tied to oil, fertilizer, or resources perceived to be in short supply. Bonds did not provide much of a buffer if any, as inflation fears put pressure on rates. Gold dropped as did most other metals. Volatility as measured by VIX just kept on creeping higher all month (with the exception of some snap back days like today).

I found that my own temperament was calm. The systems I designed lightened up during the month as % stop or time stop signals were hit, and I didn’t second guess the exit signals, I just took them and moved on.

The design of my own systems, and trading them in real time has resulted in a quiet, cautious confidence that these systems are doing what they are supposed to be doing, and by design, will produce entry signals when it is the right time. Until that time, there is not much else to do than to just wait, and not overthink or over-do things.

I hope the above is helpful to any and all readers. Until next time.